According to China’s gross domestic product (GDP) accounting and data release system, annual GDP accounting includes two steps: preliminary accounting and final verification. Recently, according to the statistical annual report of the National Bureau of Statistics, the final accounts of the Ministry of Finance and the annual financial data of relevant departments, the National Bureau of Statistics has finally verified the 2017 GDP data, and the main results are as follows:

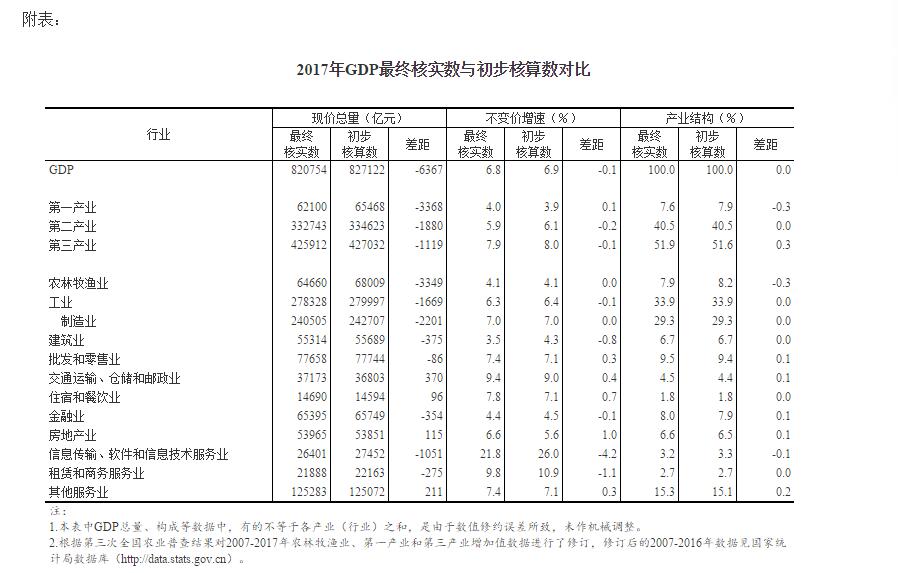

After final verification, in 2017, the total current GDP was 82,075.4 billion yuan, a decrease of 636.7 billion yuan compared with the preliminary accounting; Calculated at constant prices, it increased by 6.8% over the previous year and decreased by 0.1 percentage point compared with the preliminary accounting. See the attached table for the data of three industries and industries.

It is hereby announced.

Attached Table: Comparison between the Final Verification and Preliminary Accounting of GDP in 2017

Attachment: China GDP Annual Accounting Description

National Bureau of Statistics(NBS)

January 18, 2019

Attachment:

China GDP Annual Accounting Description

1. Overview of annual GDP accounting

1.1 Basic concepts

GDP is the final result of the production activities of all permanent units in a country in a certain period of time. GDP is the core index of national economic accounting, and it is also an important index to measure a country’s economic situation and development level.

There are three methods of GDP accounting, namely, production method, income method and expenditure method, which reflect the results of national economic production activities from different angles. Production method is a method to get added value by excluding intermediate goods and services from the value of goods and services created in the production process. The formula for calculating the added value of production method in various industries of national economy is as follows: added value = total output-intermediate input. Add up the added value of production method in various industries of the national economy to get the GDP of production method. The income method is to account for the results of production activities from the perspective of income generated by the production process. According to this calculation method, the added value consists of four parts: workers’ remuneration, net production tax, depreciation of fixed assets and operating surplus. The calculation formula is: added value = remuneration of workers+net production tax+depreciation of fixed assets+operating surplus. The sum of the added value of income method in all industries of the national economy is equal to the gross domestic product of income method. Expenditure method is a method to calculate the gross domestic product from the perspective of the final use of production activities. Final use includes final consumption expenditure, total capital formation and net export of goods and services.

Constant-price GDP is to convert GDP calculated at current price into value calculated at a fixed base period price, so as to eliminate the influence of price change factors and make the values in different periods comparable.

1.2 Accounting Scope

1.2.1 Production scope

The production scope of GDP accounting includes the following four parts: first, the production of goods or services provided or prepared by producers to other units; Second, the self-sufficient production of all goods formed by producers for their final consumption or fixed capital; Third, the self-sufficient production of knowledge carrier products by producers for their final consumption or the formation of fixed capital, but it does not include similar activities undertaken by household departments; Fourth, the housing services provided by self-owned houses and the self-sufficient production of family and personal services provided by paid family service personnel. The production scope does not include unpaid family and personal services, natural activities without unit control (such as the natural growth of wild, uncultivated forests, wild fruits or berries, and the natural growth of fish in the high seas).

1.2.2 Main scope of production activities

The main scope of GDP production activities includes all permanent units with economic interest centers within the economic territory of China. The annual GDP data in this report is the national data accounted by the National Bureau of Statistics, excluding the regional GDP data of Hongkong, Macao Special Administrative Region and Taiwan Province.

1.3 Accounting Unit

GDP accounting mainly takes corporate units as accounting units. In accounting, corporate units are divided into different industries according to their main activities, and the added value of each industry is calculated separately, and then the added value of each industry is summarized to get GDP.

1.4 Accounting Steps

According to the requirements of the timeliness of GDP accounting, China’s annual GDP should be accounted for twice, the first is the preliminary accounting of GDP, and the second is the final verification of GDP, and the results of each accounting will change.

1.4.1 Preliminary accounting

Since China’s quarterly GDP accounting adopts the cumulative accounting method before 2015, the preliminary accounting number of GDP in the first four quarters is the preliminary accounting number of annual GDP. From the third quarter of 2015, China’s quarterly GDP accounting was changed to quarterly accounting, that is, the GDP data of the first quarter, the second quarter, the third quarter and the fourth quarter of each year were calculated respectively, and the preliminary annual GDP accounting was obtained by adding the quarterly GDP data. The preliminary accounting of annual GDP shall be completed before January 20th of the following year.

1.4.2 Final verification

The final verification of annual GDP is completed in January of the following year. The reason for the final verification of annual GDP is that more comprehensive and reliable basic data have been obtained, including the professional statistical annual report of the National Bureau of Statistics, the annual financial statistics of departments, and the financial final accounts. Using these data, the added value is calculated by industry using production method or income method.

1.5 Legal basis and system provisions

GDP accounting strictly abides by the provisions of the Statistics Law of the People’s Republic of China. At present, China’s GDP is calculated according to the requirements of China National Economic Accounting System (2016), which adopts the basic accounting principles, contents and methods of the United Nations National Accounts System (2008).

1.6 confidentiality

According to Article 9 of Chapter I of the Statistics Law of the People’s Republic of China, statistical institutions and statisticians shall keep confidential the state secrets, business secrets and personal information they know in their statistical work.

National accountants keep the unpublished professional statistical data and administrative records strictly confidential when conducting GDP accounting, and also keep the current GDP data strictly confidential before the release of GDP accounting data.

1.7 User demand

Domestic users of annual GDP data are mainly government departments, research institutions, universities, industry associations, media and the public. In addition, the National Bureau of Statistics regularly provides China’s annual GDP data to international organizations such as the United Nations, the International Monetary Fund, the Organization for Economic Cooperation and Development, and the Asian Development Bank.

2. Annual GDP accounting method

2.1 classification system

In the annual GDP accounting, the industry classification is based on the China national economy industry classification standard and the third industry classification standard, and two classification methods are adopted.

The first classification is the national economic industry classification, which adopts the National Economic Industry Classification (GB/T 4754-2011) issued by the National Standards Administration in 2011. Two-level classification is adopted in actual accounting.

The first-level classification is based on the categories in the national economic industry classification, and it is divided into 11 industries, including agriculture, forestry, animal husbandry, fishery, industry, construction, wholesale and retail, transportation, warehousing and postal services, accommodation and catering, finance, real estate, information transmission, software and information technology services, leasing and business services, and other services. Among them, the industry includes mining, manufacturing, electricity, heat, gas and water production and supply industries; Other service industries include scientific research and technical services, water conservancy, environment and public facilities management, residential services, repairs and other services, education, health and social work, culture, sports and entertainment, public management, social security and social organizations. On the basis of the first classification, the second classification is subdivided into industry categories.

The difference between the industry classification of the preliminary accounting of annual GDP and the industry classification of the final verification of annual GDP is mainly due to the different degree of refinement of the second-level classification.

The second classification is the classification of tertiary industries, which is divided into primary industry, secondary industry and tertiary industry according to the Regulation on the Classification of Tertiary Industries formulated by the National Bureau of Statistics in 2012. The primary industry refers to agriculture, forestry, animal husbandry and fishery (excluding agriculture, forestry, animal husbandry and fishery services); The secondary industry refers to mining (excluding auxiliary mining activities), manufacturing (excluding metal products, machinery and equipment repair), electricity, heat, gas and water production and supply, and construction; The tertiary industry, namely the service industry, refers to other industries except the primary industry and the secondary industry (excluding international organizations).

2.2 Sources of information

The preliminary accounting of annual GDP adopts quarterly GDP accounting methods and data sources, and only the data sources of final verification of annual GDP are introduced here.

First, the national statistical survey data refers to all kinds of annual report data obtained from the statistical survey conducted by the national statistical system, including: agricultural, forestry, animal husbandry and fishery, industry, construction, wholesale and retail, accommodation and catering, real estate, service industries above designated size, household survey data, population and labor wage statistics, and price statistics.

Second, the annual financial statistics of the department refers to the annual financial statistics of the industry that are uniformly formulated by the National Bureau of Statistics and collected by relevant administrative departments and some state-owned enterprises, such as the annual financial statistics of affiliated enterprises or institutions summarized by the Ministry of Communications, the Health Planning Commission and Sinopec Group Corporation.

The third is the financial final accounts, which refers to the financial final accounts compiled by the Ministry of Finance and the financial final accounts of administrative institutions affiliated to the central department.

Fourth, the administrative records of the administrative departments, mainly including the relevant data of the State Administration of Taxation, the People’s Bank of China, the China Insurance Regulatory Commission, the China Securities Regulatory Commission and other administrative departments, such as the credit receipts and payments in local and foreign currencies of financial institutions of the People’s Bank of China, and the tax information of the State Administration of Taxation by industry.

2.3 accounting methods

The annual GDP preliminary accounting method is the same as the quarterly GDP accounting method, so I won’t repeat it here. The following introduces the final verification method of annual GDP.

2.3.1 Accounting method of current value-added

The current added value of agriculture, forestry, animal husbandry and fishery is calculated by production method, and the current added value of other industries is calculated by income method.

2.3.2 Accounting method of constant price added value

The added value of constant prices by industry is calculated by the fixed base period method. At present, the base period is changed every five years, and the base period of constant price added value from 2016 to 2020 is 2015.

Annual constant price GDP accounting mainly adopts price index reduction method and volume index extrapolation method.

2.3.2.1 price index reduction method

Use the relevant price index to directly reduce the current price added value and calculate the constant price added value. The calculation formula is:

Constant price added value of an industry = current price added value of the industry ÷ price index of the industry.

Extrapolation method of 2.3.2.2 mass index

Calculate the growth rate of constant price added value by using the growth rate of related material indexes, and then calculate the current constant price added value of the industry by using the constant price added value of the previous year and the calculated growth rate of constant price added value. The calculation formula is:

Constant price added value of an industry = constant price added value of the industry in the previous year × (1+growth rate of constant price added value of the industry)

Among them, the growth rate of constant price added value is determined according to the growth rate of relevant volume indicators (such as transportation turnover, employees, etc.) in this period, and the quantitative relationship between the growth rate of constant price added value in previous years and the growth rate of relevant volume indicators.

3. Revision of annual GDP data

3.1 the necessity of revision

The preliminary accounting of annual GDP is very time-sensitive, and it is generally published about 20 days after the year. At this time, because a large number of annual financial data can’t meet the requirements of annual GDP accounting in time, the basic data on which the preliminary annual GDP figures are calculated are all monthly data and quarterly data, and the annual GDP data calculated according to this has a great calculation component. After that, with the continuous increase of basic data, especially the annual financial data, according to the common practice of various countries, GDP data should be revised in a timely manner based on more comprehensive and reliable basic data.

3.2 Revision procedure

According to the latest reform of GDP accounting and data release system of National Bureau of Statistics, China’s annual GDP accounting is divided into two steps: preliminary accounting and final verification, and final verification is the revision of preliminary accounting data. After the national economic census is carried out and new basic data that have great influence on GDP data are found, or the calculation method and classification standard have changed, the annual GDP historical data should also be revised.

4. Annual GDP data quality evaluation

4.1 Evaluation of basic data

For the professional statistical data and administrative record data used in GDP accounting, the relevant professional statistical departments and administrative departments will test their quality to ensure that the data reasonably reflect the actual situation of economic development. When the GDP accounting department gets these basic data, it will test the integrity, comparability and accuracy of the data again to ensure that these data meet the concepts and requirements of GDP accounting.

4.2 Evaluation of accounting methods

In the GDP accounting, the GDP accounting department will revise China’s annual GDP accounting method according to the constantly developing economic reality of China and the constantly improving international standards of national economic accounting, so as to ensure the rationality of the accounting method.

4.3 Evaluation of accounting results

After calculating the annual GDP data, it is necessary to test the coordination of GDP and its sub-data, GDP and other accounting data, GDP and related professional statistics and departmental statistics to ensure the coordination and matching of GDP data and other major related data.

4.4 Comparability of data

4.4.1 International comparability

The China National Economic Accounting System (2016) adopted the basic accounting principles, contents and methods of the United Nations National Accounts System (2008), so the GDP data is internationally comparable.

4.4.2 Comparability of time series

After a nationwide census or changes in calculation methods and classification standards, not only the GDP data of the current year are recalculated, but also the historical GDP data are revised. Therefore, the published annual GDP data time series since 1952 is comparable.

5. Annual GDP data release

5.1 Release time

The preliminary accounting data of annual GDP is generally released around January 20 of the following year, and the final verification data of annual GDP is released in January of the following year.

5.2 Release method

The preliminary accounting figures of annual GDP are published in the annual press conference on the operation of the national economy, the website of the National Bureau of Statistics, and the "China Economic Prosperity Monthly Report"; The final verification number of annual GDP is published on the website of the National Bureau of Statistics in the form of an announcement by the National Bureau of Statistics; At the same time, the final verification number of annual GDP is also published in the Statistical Abstract of China and the Statistical Yearbook of China every other year; The national statistical database will be updated simultaneously.

关于作者